Blank Nebraska 14N PDF Template

Blank Nebraska 14N PDF Template

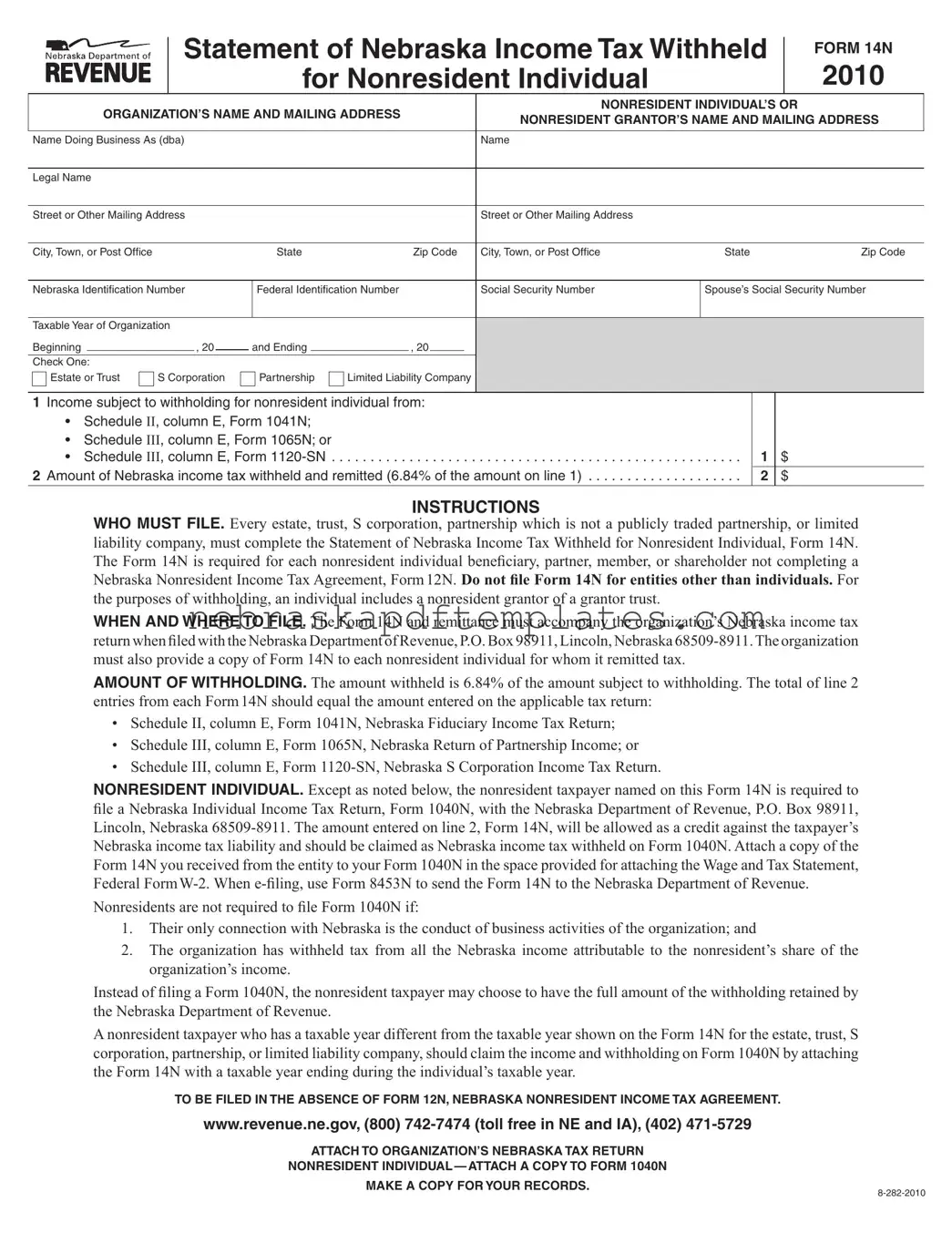

When filling out the Nebraska 14N form, there are important dos and don’ts to keep in mind. Following these guidelines can help ensure that your form is completed correctly.

Incomplete Information: Failing to provide all necessary details, such as the organization’s name, mailing address, or the nonresident individual’s information, can lead to delays or rejections.

Incorrect Identification Numbers: Entering wrong Nebraska or Federal identification numbers can create significant issues. It is crucial to double-check these numbers for accuracy.

Improper Tax Calculation: Miscalculating the amount of Nebraska income tax withheld, which should be 6.84% of the income subject to withholding, can result in underpayment or overpayment.

Failure to File Timely: Not submitting the Form 14N along with the organization’s Nebraska income tax return by the deadline may lead to penalties. Timeliness is essential.

Neglecting to Provide Copies: Organizations must provide a copy of Form 14N to each nonresident individual. Failing to do so can create confusion and issues for the taxpayer.

Ignoring the Need for Attachments: When filing Form 1040N, the nonresident taxpayer must attach a copy of Form 14N. Not including this can affect the credit claimed against Nebraska income tax liability.

| Fact Name | Fact Description |

|---|---|

| Purpose of Form | The Nebraska 14N form serves as a Statement of Nebraska Income Tax Withheld for Nonresident Individuals. It is used to report income tax withheld from nonresident beneficiaries, partners, members, or shareholders. |

| Who Must File | Filing is required for every estate, trust, S corporation, partnership (not publicly traded), or limited liability company that has nonresident individuals receiving income. It is not applicable to entities other than individuals. |

| Withholding Rate | The amount of Nebraska income tax withheld is set at 6.84% of the income subject to withholding, which is reported on the form. |

| Filing Instructions | Form 14N must be submitted along with the organization’s Nebraska income tax return to the Nebraska Department of Revenue. A copy should also be provided to each nonresident individual for whom tax has been withheld. |

| Nonresident Individual Requirements | Nonresident individuals must file a Nebraska Individual Income Tax Return, Form 1040N, unless their only connection to Nebraska is through business activities of the organization, and tax has been withheld from all applicable income. |

| Governing Law | The Nebraska 14N form is governed by Nebraska Revised Statutes, specifically those related to income tax withholding and nonresident taxation. |

Misconceptions about the Nebraska 14N form can lead to confusion and potential errors in tax reporting. Below are seven common misconceptions along with clarifications to help individuals understand their obligations.

Understanding these misconceptions can help ensure compliance with Nebraska tax laws and facilitate accurate tax reporting for nonresident individuals.

The Nebraska 14N form is used to report the income tax withheld for nonresident individuals, including beneficiaries, partners, members, or shareholders of estates, trusts, S corporations, partnerships, and limited liability companies. It ensures that the appropriate amount of Nebraska income tax is remitted to the state on behalf of these nonresident individuals.

Every estate, trust, S corporation, partnership (not publicly traded), or limited liability company must complete the Nebraska 14N form for each nonresident individual for whom tax has been withheld. This includes nonresident grantors of grantor trusts. Entities should not file this form for individuals who have completed a Nebraska Nonresident Income Tax Agreement, Form 12N.

The Nebraska 14N form must be filed along with the organization’s Nebraska income tax return. It should be submitted to the Nebraska Department of Revenue at P.O. Box 98911, Lincoln, Nebraska 68509-8911. Additionally, a copy of the form must be provided to each nonresident individual for whom tax has been remitted.

The withholding amount is calculated at a rate of 6.84% of the income subject to withholding reported on the form. The total of the withholding amounts from each Nebraska 14N form must match the amounts reported on the applicable tax returns, such as Schedule II of Form 1041N or Schedule III of Form 1065N and Form 1120-SN.

The Nebraska 14N form, officially known as the Statement of Nebraska Income Tax Withheld for Nonresident Individual, shares similarities with several other tax-related documents. Each of these forms serves a unique purpose but often overlaps in function, particularly regarding income tax withholding for nonresidents. Below is a list of documents that are similar to the Nebraska 14N form:

Understanding these forms can help nonresidents navigate their tax obligations in Nebraska more effectively. Each document plays a role in ensuring compliance with state tax laws.

The Nebraska 14N form is essential for reporting the income tax withheld from nonresident individuals by certain organizations. Alongside this form, several other documents may be required to ensure proper tax reporting and compliance. Below is a list of related forms and documents that are often used in conjunction with the Nebraska 14N form.

Understanding these forms and their purposes can help ensure compliance with Nebraska tax regulations. Each document plays a role in the overall process of reporting income and tax liabilities for nonresident individuals and the organizations that manage their income. Properly completing and submitting these forms is crucial for avoiding potential issues with tax authorities.

Notary Prices - The state relies on the bond to uphold the legal framework within which notaries operate.

To comply with Missouri tax regulations, employers must navigate the complexities of reporting withheld income taxes, which is where the Mo 941 form becomes essential. This form not only captures vital business information but also ensures that all necessary details regarding withheld amounts and credits are accurately reported. Timely submission of the MO-941 form is crucial for maintaining compliance and avoiding potential penalties.

Are Blue Lights on Cars Illegal - Emergency lights enhance visibility and safety for both the operator and the public.