Blank Nebraska 17 PDF Template

Blank Nebraska 17 PDF Template

When filling out the Nebraska 17 form, it is essential to follow specific guidelines to ensure accuracy and compliance. Here’s a list of things you should and shouldn't do:

By adhering to these guidelines, you can help ensure that the process runs smoothly and complies with Nebraska tax regulations.

Incomplete Information: Failing to provide all required details, such as the name and address of the prime contractor or the governmental unit, can lead to delays or rejection of the form.

Incorrect Dates: Entering an ineffective or expired date for the appointment or delegation can invalidate the form. Always ensure that the effective and expiration dates are accurate and clearly stated.

Missing Exemption Number: Exempt organizations must include their Nebraska Sales and Use Tax Exemption number. Omitting this information can result in the form being deemed incomplete.

Improper Delegation: The prime contractor must delegate authority to each subcontractor using a completed Form 17. Failing to provide proper documentation for delegation can lead to tax liabilities.

Failure to Retain Copies: Not retaining a copy of the completed form can create issues later. Both the governmental unit and the prime contractor should keep their respective copies for records.

Ignoring Filing Instructions: Not following the specific filing instructions outlined in the form can lead to complications. Ensure that all steps are adhered to, including when and where to file the form.

| Fact Name | Details |

|---|---|

| Form Title | Nebraska Department of Revenue Purchasing Agent Appointment | Form 17 |

| Governing Law | This form is governed by Nebraska sales and use tax laws. |

| Purpose | It allows a governmental unit or exempt organization to appoint a prime contractor as its agent for purchasing building materials tax-exempt. |

| Who Must File | Any exempt governmental unit or organization must file this form to appoint a prime contractor. |

| Effective Dates | The form requires an effective date and an expiration date for the appointment. |

| Exemption Number | Exempt organizations must provide their Nebraska Exemption Number on the form. |

| Delegation of Authority | The prime contractor can delegate purchasing authority to subcontractors through this form. |

| Filing Requirements | A copy must be retained by the governmental unit, while the original stays with the prime contractor. |

| Tax Payment Condition | Purchases made under this appointment must be tax-exempt only if paid for by the governmental unit or its contractor. |

| Refund Eligibility | If an exempt organization is not licensed at the time of construction, it cannot issue this form but may apply for a tax refund later. |

Misconceptions about the Nebraska 17 form can lead to confusion for contractors and exempt organizations alike. Here are nine common misunderstandings, along with clarifications to help you navigate the process more effectively.

Understanding these misconceptions can help ensure compliance with Nebraska tax laws and streamline the purchasing process for construction projects. Always consult the Nebraska Department of Revenue for the most accurate and up-to-date information.

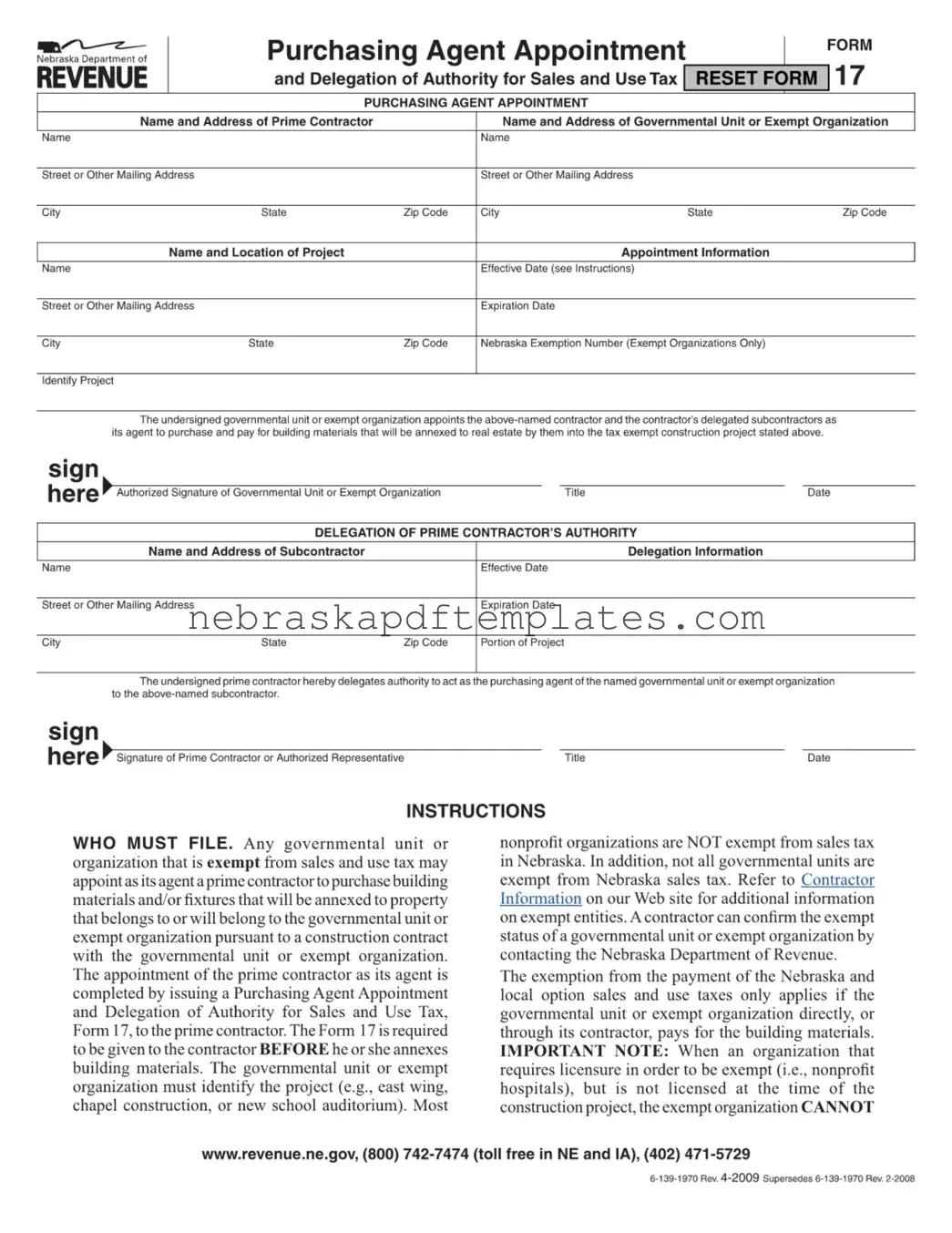

The Nebraska 17 form, also known as the Purchasing Agent Appointment and Delegation of Authority for Sales and Use Tax, is a document used by governmental units or exempt organizations in Nebraska. It allows these entities to appoint a prime contractor as their purchasing agent. This appointment enables the contractor to purchase building materials and fixtures for construction projects that will be annexed to property owned or to be owned by the governmental unit or exempt organization without incurring sales tax.

Any governmental unit or organization that is exempt from sales and use tax in Nebraska may file the Nebraska 17 form. This includes entities that have a construction contract with a prime contractor. It is important to note that not all governmental units or nonprofit organizations are exempt from sales tax. Therefore, it is advisable to verify the exempt status by contacting the Nebraska Department of Revenue.

The Nebraska 17 form must be completed and issued to the prime contractor before any building materials are annexed to the project. If the form is not provided prior to the annexation, the contractor will be responsible for paying the sales and use taxes. The governmental unit or exempt organization may then seek a refund of the taxes paid by the contractor.

A copy of the completed Nebraska 17 form should be retained by the governmental unit or exempt organization that issues the form. The original form must be kept by the prime contractor. If the prime contractor delegates authority to any subcontractors, copies of the form must be made for them as well.

The Nebraska 17 form requires several key pieces of information, including:

Accurate completion of this information is essential for the form to be valid.

Yes, a prime contractor can delegate authority to act as a purchasing agent to a subcontractor. The prime contractor must complete a separate Nebraska 17 form for each subcontractor who is granted this authority. The subcontractor must retain a copy of the form for their records, and copies must also be provided to the governmental unit or exempt organization.

If the construction project is not completed within the effective and expiration dates specified on the Nebraska 17 form, the governmental unit or exempt organization must issue a new form to extend the appointment. The original form will not remain valid beyond the expiration date, and any purchases made after this date will require payment of sales tax.

The Exempt Sale Certificate, specifically Form 13, must be provided by the prime contractor to any subcontractor operating as an Option 1 contractor. This certificate, along with a completed Nebraska 17 form, allows the subcontractor to avoid charging sales tax on materials annexed to the specific project. If these forms are not provided, the subcontractor is required to collect and remit sales tax on the applicable materials.

Power of Attorney (POA): Similar to the Nebraska 17 form, a Power of Attorney allows one party to act on behalf of another. It grants authority to the agent to make decisions and take actions regarding specified matters, often including financial transactions.

Purchase Order (PO): A Purchase Order is a document issued by a buyer to a seller, indicating the products, quantities, and agreed prices for goods or services. Like the Nebraska 17, it formalizes a transaction and outlines the responsibilities of both parties.

Contractor Agreement: This document outlines the terms and conditions between a contractor and a client. Similar to the Nebraska 17, it specifies roles, responsibilities, and the scope of work to be performed.

Delegation of Authority Form: This form allows a principal to delegate authority to another individual. Much like the Nebraska 17, it specifies who is authorized to act on behalf of the principal and under what conditions.

Exemption Certificate: An Exemption Certificate is used to claim exemption from sales tax. Similar to the Nebraska 17, it serves as proof that the purchaser is exempt from tax on specific purchases.

Subcontractor Agreement: This document outlines the terms between a contractor and a subcontractor. It is akin to the Nebraska 17 in that it details the scope of work and the delegation of authority to the subcontractor.

Sales Tax Exemption Application: This application is used to request sales tax exemption status. Like the Nebraska 17, it is essential for organizations seeking to avoid sales tax on eligible purchases.

Letter of Authorization: A Letter of Authorization grants permission for one party to act on behalf of another. This is similar to the Nebraska 17, as both documents establish a formal relationship and outline the authority granted.

Durable Power of Attorney Form: To ensure your wishes are honored during incapacitation, access the comprehensive Durable Power of Attorney document that grants trusted individuals the authority to manage your affairs.

Vendor Agreement: A Vendor Agreement details the terms between a vendor and a buyer. Like the Nebraska 17, it outlines expectations and responsibilities regarding the sale of goods or services.

Construction Contract: This document outlines the agreement between a client and a contractor for a construction project. Similar to the Nebraska 17, it specifies the terms under which materials and labor will be provided.

The Nebraska 17 form is essential for governmental units and exempt organizations to appoint a prime contractor as their purchasing agent for tax-exempt construction projects. Alongside this form, several other documents are often utilized to ensure compliance and facilitate the purchasing process. Below is a list of these related forms and documents.

Understanding these forms and documents is crucial for ensuring that the purchasing process for tax-exempt projects runs smoothly. Each document serves a specific purpose in maintaining compliance with Nebraska tax laws and protecting the interests of all parties involved.

Ne Form 6 - Details about the purchased vehicle or trailer must be entered on the form.

How to Avoid Underpayment Penalty - Completing the form accurately contributes to a smoother tax filing experience with the state.

A California Residential Lease Agreement form is a legally binding document used between a landlord and a tenant to outline the terms of renting property in California. It covers essential agreements such as rent amount, deposit details, and the duration of the lease. Ensuring clarity and mutual understanding, this form safeguards both parties' interests during the rental period. For more detailed information, you can refer to this source: https://californiapdf.com/editable-residential-lease-agreement.

Ne Dhhs - Every question is carefully structured to gather essential information without unnecessary complexity.