Blank Nebraska 2210N PDF Template

Blank Nebraska 2210N PDF Template

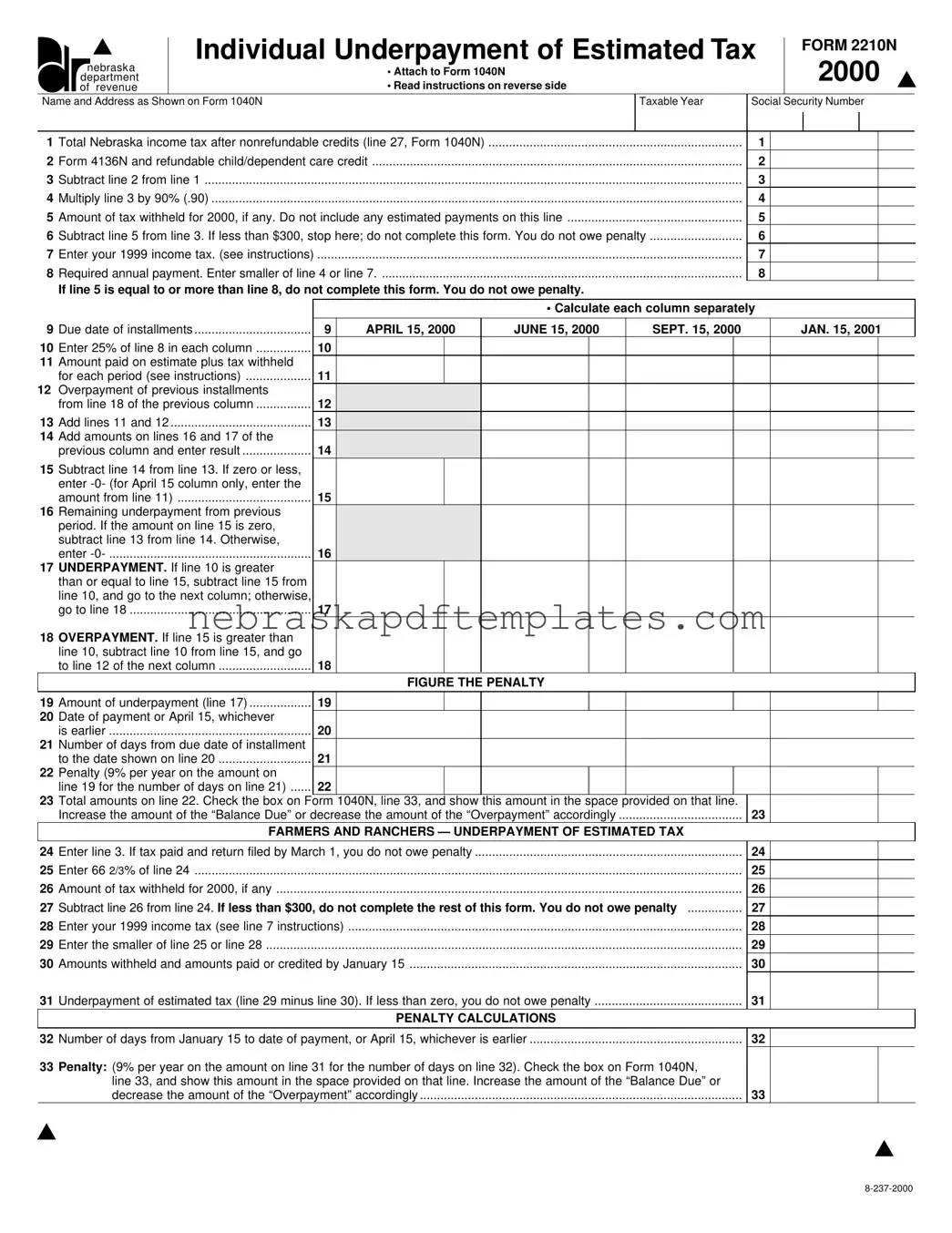

When filling out the Nebraska 2210N form, it is essential to follow specific guidelines to ensure accuracy and compliance. Here are ten things to do and avoid:

Failing to read the instructions on the reverse side of the form can lead to critical errors.

Incorrectly calculating the total Nebraska income tax after nonrefundable credits can result in an inaccurate penalty assessment.

Omitting the refundable child/dependent care credit from calculations on line 2 may lead to an inflated tax liability.

Not subtracting the amount withheld from the total tax can cause confusion regarding the actual underpayment.

Failing to check if the amount owed is less than $300 before completing the form can lead to unnecessary penalties.

Entering the wrong income tax amount from the previous year on line 7 can miscalculate the required annual payment.

Not calculating each column separately as required can lead to cumulative errors.

Forgetting to enter the correct due dates for installments can result in missed payments and penalties.

Neglecting to properly apply any overpayment from previous installments can affect the accuracy of future calculations.

Not checking the penalty calculations on lines 19 through 23 can result in incorrect reporting of the penalty amount.

| Fact Name | Fact Description |

|---|---|

| Purpose | The Nebraska 2210N form is used to calculate penalties for individuals who underpaid their estimated state income tax throughout the year. |

| Filing Requirement | Individuals must file Form 2210N if they determine that their Nebraska income tax was not sufficiently paid at any time during the year. |

| Governing Law | This form is governed by Nebraska Revised Statutes, specifically sections related to income tax and estimated tax payments. |

| Penalty Rate | The penalty for underpayment is calculated at a rate of 9% per annum on the amount of underpayment. |

| Exemptions | No penalty is owed if the total tax shown on the return minus withholding is less than $300 or if there was no tax liability in the previous year. |

| Filing Deadline | Form 2210N must be attached to the Nebraska Individual Income Tax Return, Form 1040N, and filed by the tax return deadline. |

| Installment Payments | Installment payments are due on April 15, June 15, September 15, and January 15 of the following year, based on the previous year's tax liability. |

Misconception 1: The Nebraska 2210N form is only for individuals who owe taxes.

This is not true. Even if you expect a refund, you may still need to file this form if you didn’t pay enough estimated tax during the year.

Misconception 2: You can ignore the 2210N form if you have withheld enough taxes at the end of the year.

Actually, the penalty can still apply if you didn’t pay enough estimated tax by the required due dates, even if you ultimately owe no tax when filing your return.

Misconception 3: Filing the 2210N form guarantees you will not face any penalties.

Filing the form does not automatically exempt you from penalties. You must still meet specific requirements regarding your estimated payments to avoid penalties.

Misconception 4: You can only use the 2210N form if you had a tax liability in the previous year.

This is incorrect. Even if you had no tax liability last year, you may still need to file if your tax due this year is less than $300.

Misconception 5: The penalty calculations on the 2210N form are straightforward and easy to understand.

Many find the calculations complex. It’s essential to read the instructions carefully and ensure accuracy to avoid mistakes.

Misconception 6: You must file the 2210N form with your tax return, regardless of your situation.

You only need to file it if you determine that you owe a penalty due to underpayment. If your tax situation is straightforward, you may not need it.

Misconception 7: The 2210N form applies only to regular taxpayers, not to farmers or ranchers.

Farmers and ranchers have specific rules that may exempt them from penalties if they meet certain income thresholds and file by a specific date.

Misconception 8: Completing the 2210N form is optional if you believe you will receive a refund.

It is crucial to complete the form if you determine you owe a penalty, as failing to do so can lead to additional penalties and interest.

The Nebraska 2210N form is used by individuals to calculate any underpayment of estimated state income tax for the tax year. If you did not pay enough estimated tax throughout the year or did not have enough tax withheld, you may need to complete this form to determine if you owe a penalty.

Individuals who find that their Nebraska individual income tax was not sufficiently paid at any point during the year must file this form. This includes anyone who did not meet their estimated tax payments by the required due dates or had insufficient withholding from their income.

You will not incur a penalty if one of the following applies:

To calculate your underpayment, complete the necessary lines on the form. You will compare your total tax liability to the amount you have paid through withholding and estimated payments. If the difference is less than $300, you do not need to complete the form.

The penalty for underpayment is calculated at a rate of 9% per year on the amount of underpayment for the number of days it remains unpaid. This calculation is done separately for each installment due date.

The 2210N form must be attached to your Nebraska Individual Income Tax Return, Form 1040N, which is typically due on April 15. If you are filing for a fiscal year, the due dates will vary based on your specific fiscal calendar.

If you overpaid your estimated tax, any excess amount can be credited towards your next installment. You will need to complete the relevant lines on the form to ensure this overpayment is accurately reflected.

Yes, if your gross income from farming, ranching, or fishing constitutes at least two-thirds of your total annual gross income, and you file your Form 1040N and pay your Nebraska income tax by March 1, you are exempt from penalties for underpayment and do not need to file Form 2210N.

If you believe the penalty should not apply due to special circumstances, you can attach a statement to your form explaining your situation. This might include issues like a casualty or disaster that affected your ability to pay, or if you retired or became disabled.

The Nebraska 2210N form is used to calculate penalties for underpayment of estimated tax. It shares similarities with several other tax-related documents. Here are five forms that are comparable to the Nebraska 2210N, along with explanations of how they are similar:

The Nebraska 2210N form is essential for individuals who may have underpaid their estimated tax throughout the year. To ensure accurate filing and compliance with tax obligations, several other forms and documents are often utilized in conjunction with the 2210N. Below is a list of these commonly associated documents, along with brief descriptions of their purposes.

Understanding the interplay between these forms and the Nebraska 2210N can significantly ease the tax filing process. By ensuring all necessary documents are completed and submitted, individuals can avoid penalties and ensure compliance with tax regulations.

Accessnebraska - Penalties apply for late filing, including 10% of unpaid tax or a minimum of $25.

For individuals seeking guidance on the necessary documentation, the "accurate Mobile Home Bill of Sale" is crucial. This form not only facilitates the transfer of ownership but also provides essential legal safeguards for both parties involved. To access the form directly, visit the official Mobile Home Bill of Sale form.

Nebraska Title Application - Declaring the types of vehicles and trailers the applicant is authorized to sell is essential.