Blank Nebraska 33 PDF Template

Blank Nebraska 33 PDF Template

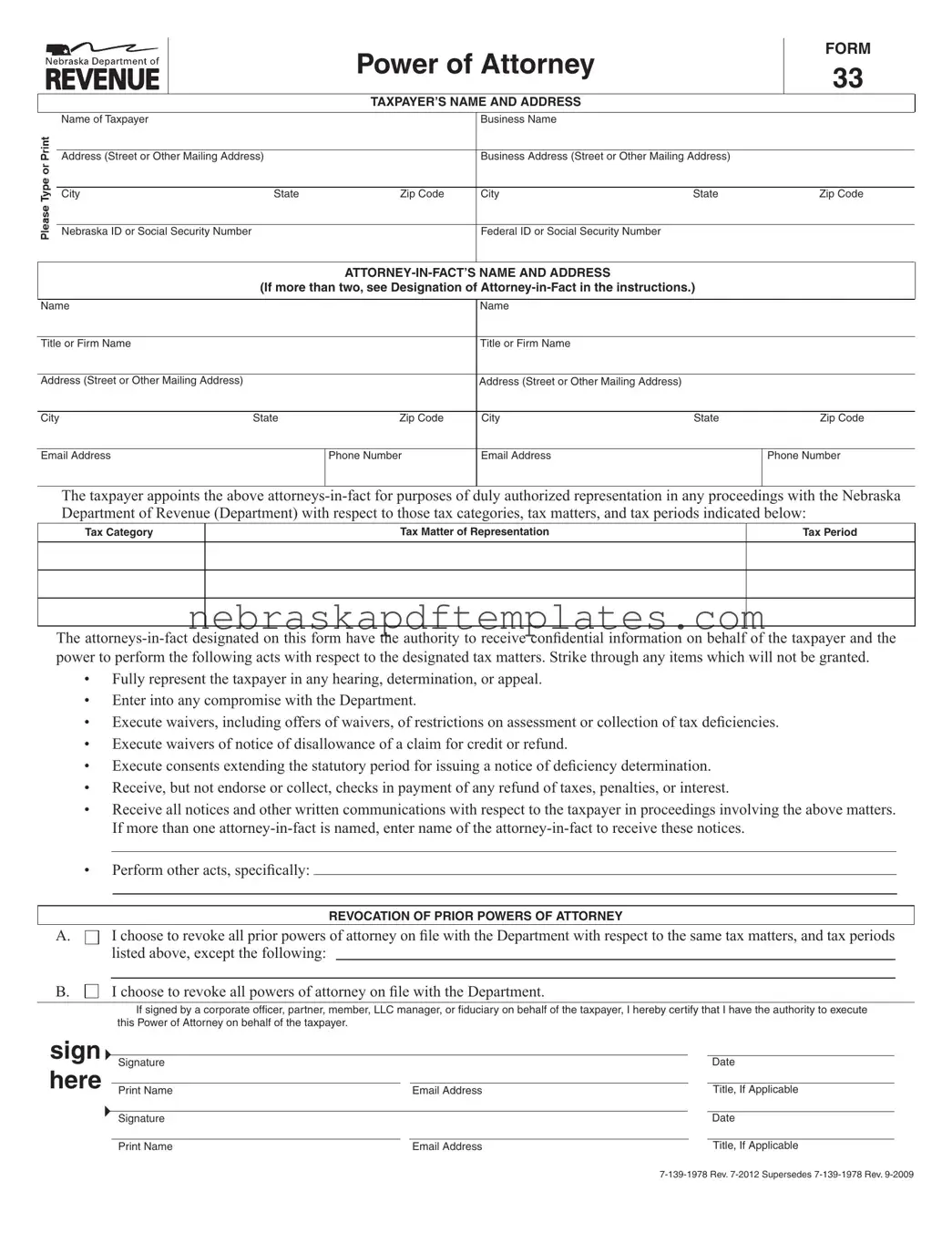

When filling out the Nebraska 33 form, consider the following guidelines:

Incomplete Information: One of the most common mistakes is not filling out all required fields. This includes the taxpayer's name, address, and identification numbers. Omitting any of these details can lead to delays in processing.

Incorrect Designation of Attorney-in-Fact: Many people fail to accurately designate their attorney-in-fact. It is crucial to provide the correct names and addresses of those authorized to act on behalf of the taxpayer. If there are multiple attorneys, ensure that all are listed correctly.

Failure to Specify Tax Matters: The form requires taxpayers to specify the tax categories and periods for which the power of attorney is granted. A vague or incomplete description can result in confusion and limit the authority of the designated representatives.

Neglecting to Sign the Form: A signature is mandatory for the form to be valid. Without a signature, the form cannot be processed. Additionally, if the taxpayer is married and filing jointly, both spouses must sign the form.

Not Revoking Previous Powers of Attorney: If there are prior powers of attorney on file, failing to properly revoke them can create complications. Taxpayers must clearly indicate whether they wish to revoke all previous powers or only specific ones.

| Fact Name | Fact Details |

|---|---|

| Purpose of Form | The Nebraska 33 form is used to appoint an attorney-in-fact for representation in tax matters before the Nebraska Department of Revenue. |

| Governing Law | This form operates under the tax laws of the State of Nebraska, particularly in accordance with Nebraska Revised Statutes. |

| Taxpayer Information | Taxpayers must provide their name, address, and either a Social Security number or Nebraska ID number on the form. |

| Attorney-in-Fact | Taxpayers can appoint up to two attorneys-in-fact, with additional names included on a separate sheet if needed. |

| Authorized Acts | The form allows attorneys-in-fact to perform various acts, including representing the taxpayer in hearings and entering compromises with the Department. |

| Revocation of Powers | Taxpayers can revoke prior powers of attorney by selecting either Box A or Box B on the form, specifying which powers remain in effect if necessary. |

| Filing Instructions | The completed form can be filed via email, fax, or mail to the Nebraska Department of Revenue at any time. |

| Signature Requirements | Both spouses must sign if filing jointly. If only one spouse signs, a separate form must be completed by the other spouse. |

Misconceptions about the Nebraska 33 form can lead to confusion regarding its use and requirements. Here are five common misconceptions:

The Nebraska 33 form is a Power of Attorney document specifically designed for taxpayers who wish to appoint another individual or entity to represent them in matters before the Nebraska Department of Revenue. This form allows the appointed representatives, known as attorneys-in-fact, to receive confidential tax information and act on behalf of the taxpayer in various tax-related matters.

Any taxpayer who wants to secure representation for tax matters with the Nebraska Department of Revenue must file the Nebraska 33 form. This includes individuals, corporations, partnerships, and estates. If a taxpayer wishes to allow someone else to handle their tax issues, such as audits or appeals, they must complete this form to grant the necessary authority.

The completed Nebraska 33 form can be filed at any time. It must be submitted to the Nebraska Department of Revenue before the appointed representative can act on behalf of the taxpayer. There are multiple ways to file the form: it can be emailed to rev.poa@nebraska.gov, faxed to 402-471-5608, or mailed to the Nebraska Department of Revenue at PO Box 94818, Lincoln, NE 68509-4818.

The form requires several key pieces of information:

It is crucial that all information is accurately filled out to avoid any issues with representation.

Yes, the Nebraska 33 form includes a section for revoking prior Powers of Attorney. Taxpayers can choose to revoke all previous authorizations or only specific ones. To do this, they must check the appropriate box on the form and provide any necessary details about the prior Powers of Attorney that are to remain in effect.

If there are specific acts that the taxpayer wishes to authorize that are not included in the standard list on the Nebraska 33 form, they can do so by writing a concise statement in the designated space provided. Alternatively, a separate signed statement can be attached to the form to specify any additional authorizations.

The Nebraska 33 form is a Power of Attorney document that allows a taxpayer to designate someone to represent them in tax matters before the Nebraska Department of Revenue. Along with this form, several other documents are often utilized to ensure comprehensive representation and compliance with tax laws. Below is a list of related forms and documents that may be required or helpful in conjunction with the Nebraska 33 form.

Each of these forms serves a specific purpose in the tax process and may be necessary depending on the taxpayer's situation. Properly completing and submitting these documents can help ensure smooth interactions with the Nebraska Department of Revenue and compliance with federal tax laws.

Nebraska Vanity Plates - Longer message plates may carry additional fees and specific regulations for use and design.

To better understand the nuances of this important legal document, you can find valuable resources and editable versions at https://californiapdf.com/editable-power-of-attorney/, which provide guidance tailored to California's regulations regarding Power of Attorney forms.

The Two Most Important Criteria for Proper Notarization Are - Guidelines for handling objections during the notarization process are also provided.

Nebraska Tax Forms - Understand all filing requirements to avoid potential penalties or issues with tax compliance.