Blank Nebraska 451 PDF Template

Blank Nebraska 451 PDF Template

When filling out the Nebraska 451 form, consider the following dos and don'ts:

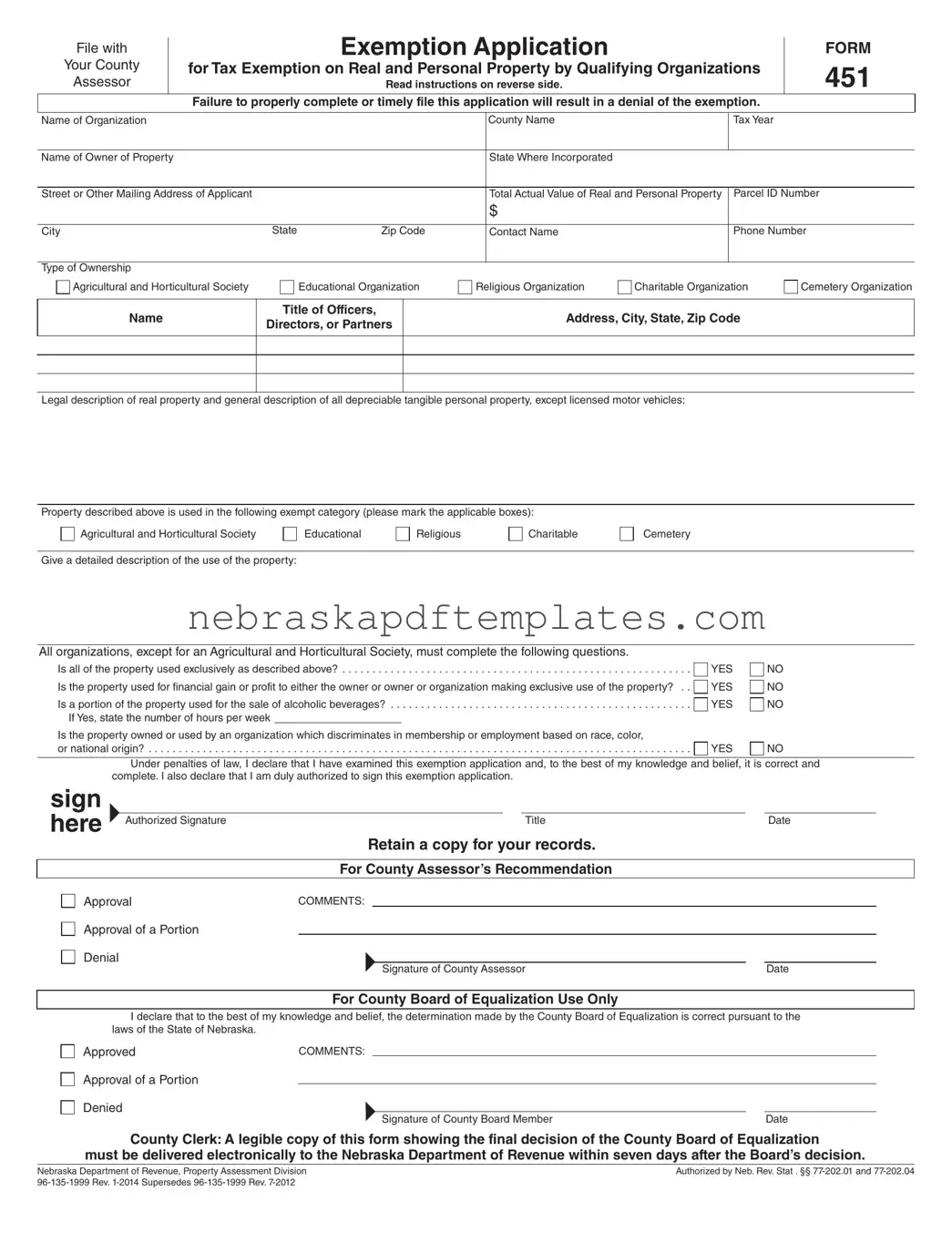

Incomplete Information: Failing to provide all required details, such as the name of the organization, county, or tax year, can lead to delays or denial of the application.

Incorrect Parcel ID Number: Entering an incorrect Parcel ID Number can cause confusion and may result in the application being processed incorrectly.

Missing Signatures: Not signing the form or having an unauthorized person sign it can invalidate the application.

Failure to Mark Exempt Categories: Not indicating the appropriate exempt categories can lead to a misunderstanding of the property’s use and purpose.

Neglecting Detailed Descriptions: Providing vague or insufficient descriptions of how the property is used may raise questions and lead to denial.

Missing the Filing Deadline: Submitting the form after the December 31 deadline can result in penalties and a loss of exemption eligibility.

Inaccurate Claims of Exclusivity: Claiming that the property is used exclusively for exempt purposes without proper justification can lead to disqualification.

Ignoring Additional Documentation: Failing to attach necessary supporting documents or additional sheets when required can hinder the application process.

| Fact Name | Description |

|---|---|

| Purpose | The Nebraska 451 form is used by qualifying organizations to apply for tax exemptions on real and personal property. |

| Filing Deadline | Organizations must file the form by December 31 of the year preceding the tax year for which the exemption is sought. |

| Governing Laws | This form is authorized by Nebraska Revised Statutes §§ 77-202.01 and 77-202.04. |

| Eligibility Criteria | To qualify, property must be owned and used exclusively for purposes such as educational, religious, charitable, or agricultural activities. |

| Consequences of Late Filing | If filed late, organizations may face a penalty of up to 10% of the tax that would have been assessed for each month the filing is delayed. |

Misconceptions about the Nebraska 451 form can lead to confusion and potential issues when applying for tax exemptions. Below are five common misconceptions, along with clarifications to help organizations navigate the process effectively.

The Nebraska 451 form is an application for tax exemption on real and personal property owned by qualifying organizations. This form is specifically designed for organizations such as educational, religious, charitable, cemetery, and agricultural societies that seek to be exempt from property taxes. To qualify, the property must be used exclusively for the stated exempt purposes and not for financial gain or profit. Organizations must file this form timely to avoid denial of the exemption.

Eligibility to file the Nebraska 451 form includes organizations that own real or depreciable tangible personal property, except licensed motor vehicles. Specifically, the following types of organizations can apply:

To qualify for the exemption, the property must be used exclusively for the organization's stated purpose and not for profit. Additionally, the organization must not discriminate in membership or employment based on race, color, or national origin.

The Nebraska 451 form must be filed with the county assessor by December 31 of the year preceding the tax year for which the exemption is sought. If an organization misses this deadline, they may file by June 30, but must also request a waiver from the county board of equalization. This waiver allows the county assessor to consider the application despite the late filing. It is crucial to adhere to these deadlines to avoid penalties and ensure the application is considered.

If the Nebraska 451 form is filed late, the organization can still submit the form by June 30, but must also submit a written request for a waiver. The county board of equalization will review the request to determine if good cause exists for the late filing. If the waiver is granted, the county assessor will evaluate the application. However, a penalty of 10% of the tax that would have been assessed may be applied for each month the application is late, with a maximum penalty of $100. It is essential to act quickly to minimize these penalties and ensure compliance.

The Nebraska 451 form is crucial for organizations seeking property tax exemptions on real and personal property. However, it is often accompanied by several other important documents that help support the exemption application process. Below are five commonly used forms and documents that organizations may need to submit alongside the Nebraska 451 form. Understanding these documents can enhance the likelihood of a successful exemption application.

By preparing these additional documents, organizations can strengthen their applications and ensure compliance with Nebraska's property tax exemption requirements. Timely and accurate submissions are essential for achieving the desired outcomes in the exemption process.

Nebraska Form 13 - Approval must be noted by an authorized representative’s signature, along with the date.

Nebraska Tax Id Number Lookup - MMP must collect and report taxes for sales they facilitate.

The California Release of Liability form is an essential tool for managing risk in various activities and agreements. By utilizing this document, parties can ensure that they are protected from potential legal claims, fostering a clearer understanding of liability. It is particularly important in contexts where harm or damage may occur, and those interested in adapting this form for their needs can find resources at californiapdf.com/editable-release-of-liability/.

Nebraska Vanity Plates - Residents of certain counties may have special access to specific message plates, adding to their local identity.