Blank Nebraska 706N PDF Template

Blank Nebraska 706N PDF Template

Filling out the Nebraska 706N form can be a complex process. Here are five common mistakes that individuals often make when completing this form:

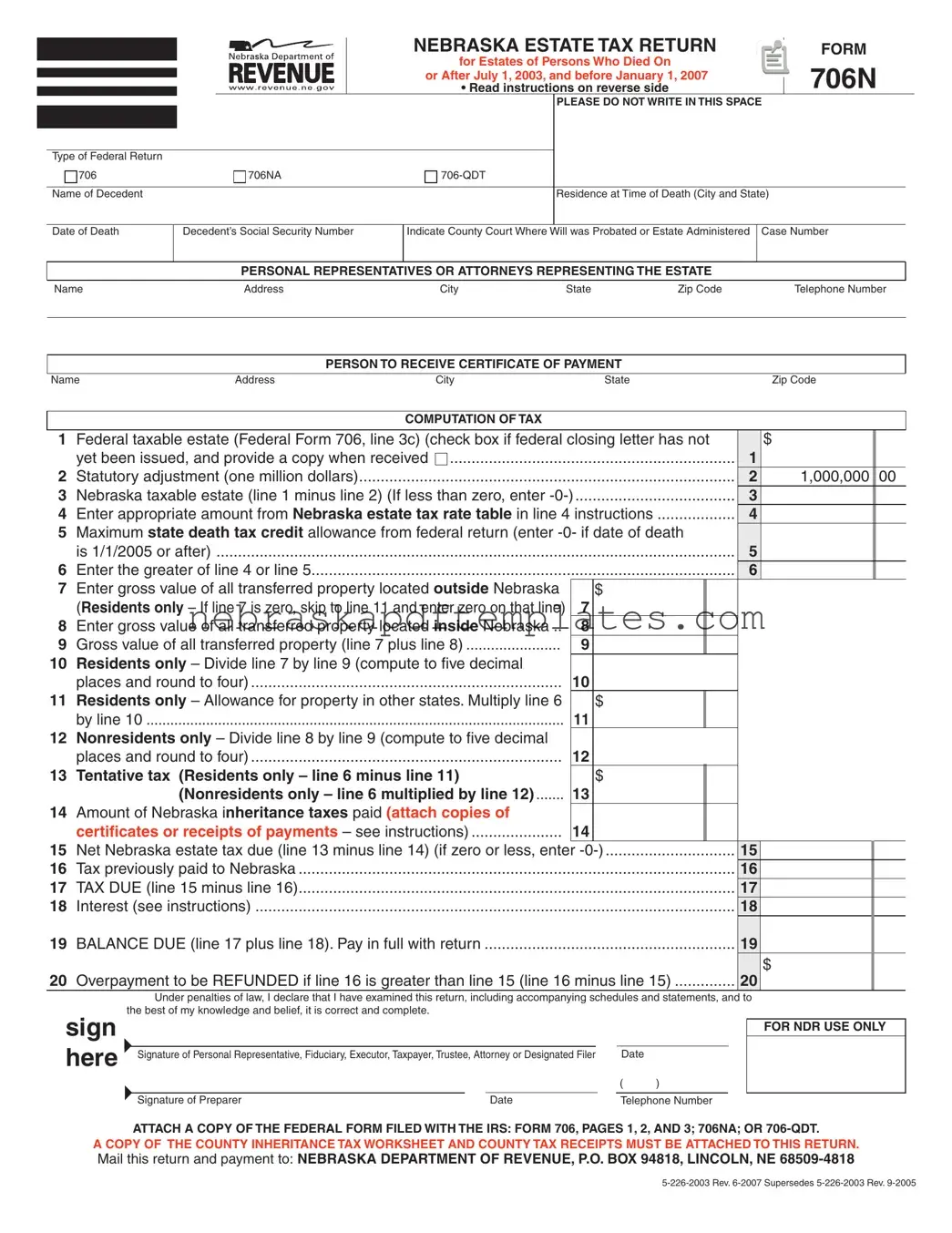

Many filers overlook the need to attach a copy of the federal Form 706, along with any inheritance tax worksheets and receipts for taxes paid. Not providing these documents can delay processing and create complications.

Some people enter an incorrect amount for the federal taxable estate on line 1. This figure must match the amount reported on the federal Form 706, line 3c. Double-checking this entry is crucial.

If a federal closing letter has not been issued, filers must check the corresponding box on line 1. Failing to do so can lead to processing issues or delays.

Errors often occur when calculating the Nebraska taxable estate on line 3. This amount should reflect the federal taxable estate minus the statutory adjustment of one million dollars. Ensure accurate calculations to avoid complications.

It’s essential for the personal representative or designated filer to sign the return. Without a signature, the form is considered incomplete, which can result in penalties or delays in processing.

By being aware of these common mistakes, individuals can take steps to ensure their Nebraska 706N form is completed accurately and submitted without unnecessary delays.

| Fact Name | Details |

|---|---|

| Purpose of Form | The Nebraska Form 706N is used to file the estate tax return for individuals who died between July 1, 2003, and January 1, 2007. |

| Governing Law | This form is governed by the Nebraska Revised Statutes, specifically under Chapter 77, which pertains to the state’s estate tax regulations. |

| Filing Deadline | The return must be filed within 12 months of the decedent's date of death. |

| Who Must File | Estates with a federal taxable estate of one million dollars or more must file this return, regardless of whether a federal return is required. |

| Required Attachments | Attach a copy of Federal Form 706, along with any necessary inheritance tax worksheets and receipts. |

| Tax Calculation | The Nebraska estate tax is calculated based on the Nebraska taxable estate, which is the federal taxable estate minus one million dollars. |

| Interest on Late Payment | If the tax due is not paid by the deadline, interest will accrue at the statutory rate from the due date until payment is made. |

| Refund of Overpayment | Any overpayment can be refunded by filing an amended return within four years of the overpayment date. |

| Certificate of Payment | A certificate evidencing payment of the Nebraska estate tax will be issued after the return has been filed and the tax paid. |

| Contact Information | For questions, individuals can visit the Nebraska Department of Revenue website or call their toll-free number for assistance. |

Misconceptions about the Nebraska 706N form can lead to confusion and potentially costly errors. Below are seven common misconceptions, along with clarifications to help ensure proper understanding and compliance.

Understanding these misconceptions can help individuals navigate the complexities of estate tax filings in Nebraska more effectively. Proper compliance with the 706N form is essential for avoiding penalties and ensuring that all obligations are met.

The Nebraska 706N form is the Estate Tax Return required for estates of individuals who passed away on or after July 1, 2003, and before January 1, 2007. This form must be filed if the estate has a federal taxable estate of one million dollars or more. It helps determine the Nebraska estate tax due based on the value of the estate and other relevant factors.

Filing the Nebraska 706N form is mandatory for estates with a federal taxable estate of one million dollars or more. This requirement applies regardless of whether a federal estate tax return (Forms 706, 706NA, or 706-QDT) is necessary. Additionally, the decedent must have been a resident of Nebraska or owned real property in the state at the time of death.

The Nebraska 706N form must be submitted within 12 months following the date of the decedent's death. It is crucial to meet this deadline to avoid potential penalties and interest on any unpaid taxes.

When completing the Nebraska 706N form, you will need to provide several pieces of information, including:

If you overpay the Nebraska estate tax, you may be eligible for a refund. To claim this refund, an amended return must be filed within four years of the overpayment or within one year of a change in the federal tax amount, whichever is later. The refund will include interest calculated at the statutory rate.

Once you have completed the Nebraska 706N form, it should be mailed to the Nebraska Department of Revenue at the following address: P.O. Box 94818, Lincoln, Nebraska 68509-4818. Be sure to include any required payments and supporting documentation to ensure your return is processed smoothly.

The Nebraska 706N form is an important document for estate tax purposes in Nebraska. It shares similarities with several other forms used in estate and inheritance tax matters. Below is a list of documents that are similar to the Nebraska 706N form, along with explanations of their similarities.

The Nebraska 706N form is a crucial document for estates of individuals who died between July 1, 2003, and January 1, 2007. When filing this return, several other forms and documents often accompany it. Each of these plays an important role in ensuring compliance with Nebraska estate tax laws.

Completing the Nebraska 706N form and its accompanying documents is essential for fulfilling estate tax obligations in Nebraska. Each document serves a specific purpose and collectively ensures that the estate is properly managed and reported to the state.

The Two Most Important Criteria for Proper Notarization Are - Key responsibilities of the Nebraska Secretary of State are articulated in relation to Notaries.

Business License Nebraska - Section A is essentially for business entities looking to resell items.

The California Vehicle Purchase Agreement form is a legal document that outlines the terms and conditions of a vehicle sale between a buyer and a seller in California. It serves to protect both parties by detailing important information such as the vehicle's price, condition, and payment method. Understanding this form is essential for anyone involved in buying or selling a vehicle in the state, and you can find a template for this agreement at My PDF Forms.

Does Nebraska Have State Tax - It simplifies the tax process for both nonresidents and the organizations they are involved with.