Blank Nebraska Sales Tax Statement PDF Template

Blank Nebraska Sales Tax Statement PDF Template

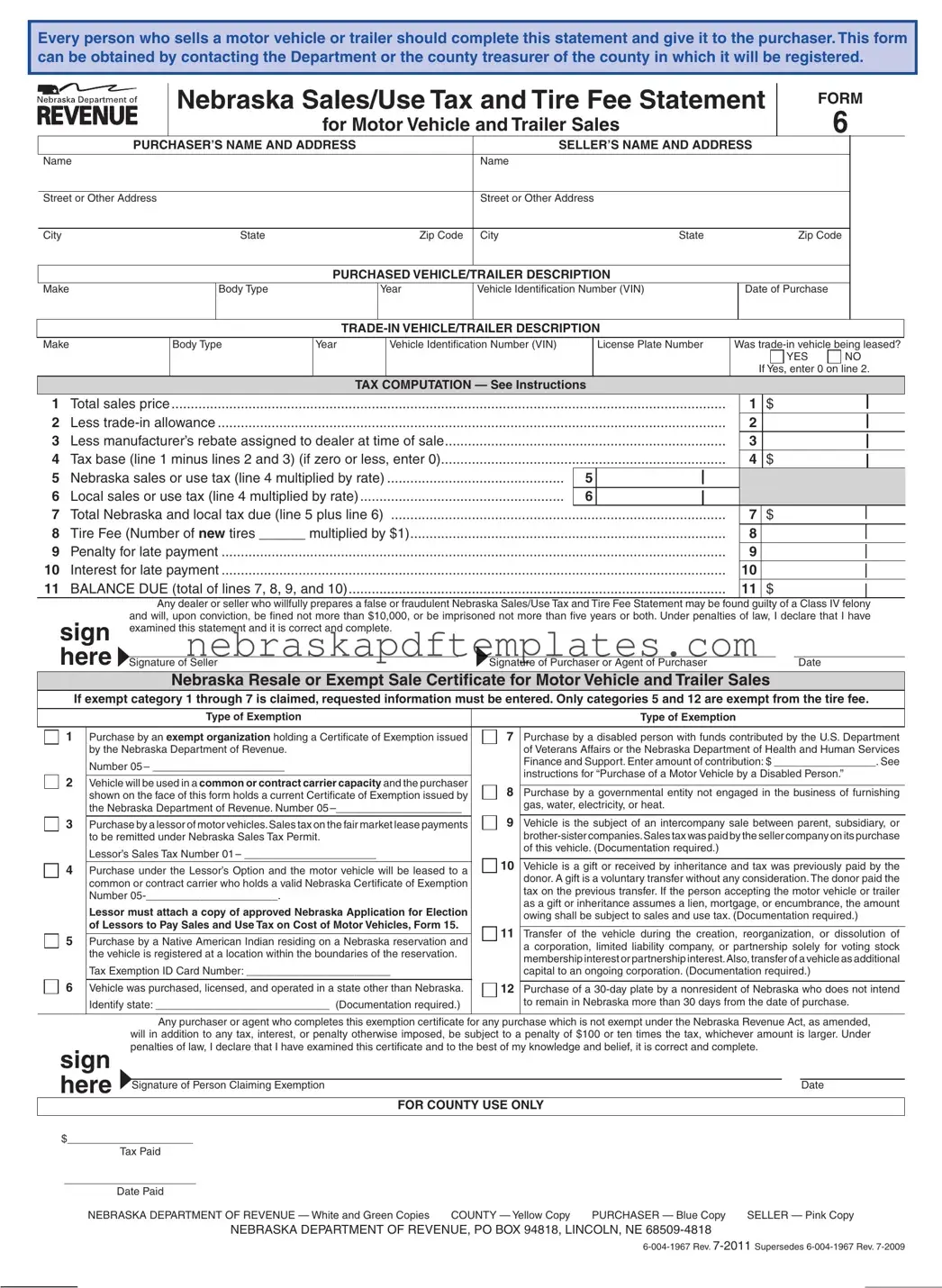

When filling out the Nebraska Sales Tax Statement form, there are several important dos and don’ts to keep in mind. This will help ensure a smooth process and avoid any potential issues.

Incorrectly filling out names and addresses: Ensure that both the purchaser's and seller's names and addresses are complete and accurate. Missing or incorrect information can delay processing.

Failing to provide vehicle details: The description of the purchased vehicle or trailer, including make, body type, year, and VIN, must be filled out completely. Omitting any of these details can lead to complications.

Miscalculating the tax base: Pay careful attention to the tax computation section. Ensure that the total sales price, trade-in allowance, and manufacturer’s rebate are accurately calculated to avoid errors in tax owed.

Not indicating trade-in details: If a trade-in vehicle is involved, it is crucial to specify its details and whether it was leased. Failing to do so can result in improper tax calculations.

Ignoring exemption requirements: If claiming an exemption, ensure that the appropriate exemption category is checked and supporting documentation is attached. Missing documentation may lead to tax assessments.

Neglecting to sign the form: Both the seller and purchaser must sign the form. A missing signature can invalidate the statement and cause delays in the registration process.

| Fact Name | Details |

|---|---|

| Purpose | This form is required for every sale of a motor vehicle or trailer in Nebraska. |

| Obtaining the Form | The form can be obtained from the Department of Revenue or the county treasurer. |

| Tax Calculation | The form includes a section for calculating Nebraska sales tax and local sales tax based on the sale price. |

| Trade-In Vehicle | If a trade-in vehicle is involved, its allowance must be deducted from the total sales price. |

| Exemptions | There are specific exemptions available, including purchases by disabled persons or governmental entities. |

| Penalties | Filing a false statement can result in severe penalties, including fines and imprisonment. |

| Deadline for Payment | Taxes and fees must be paid within 30 days of purchase to avoid penalties and interest. |

| Governing Law | This form is governed by Nebraska Revised Statutes, specifically related to sales and use tax regulations. |

Misconception 1: Only licensed dealers need to complete the Nebraska Sales Tax Statement.

This form must be completed by anyone selling a motor vehicle or trailer, not just licensed dealers. Private sellers are also responsible for filling it out and providing it to the purchaser.

Misconception 2: The form can be submitted at any time after the sale.

The completed form must be presented to the county treasurer or designated official within 30 days of the purchase date. Delays can result in penalties and interest charges.

Misconception 3: Trade-ins automatically reduce the sales tax owed.

A trade-in allowance can reduce the taxable amount, but only if properly documented. If a vehicle is leased, it may not qualify for a trade-in deduction.

Misconception 4: Sales tax is only due if the vehicle is registered in Nebraska.

Misconception 5: Exemptions from sales tax are automatic.

Exemptions must be claimed using the Nebraska Resale or Exempt Sale Certificate. Documentation supporting the exemption is required, and if it is insufficient, taxes will still be collected.

The Nebraska Sales Tax Statement form is required for every sale of a motor vehicle or trailer in Nebraska. Sellers must complete this form and provide it to the purchaser. It serves as a record of the transaction and helps ensure that the appropriate sales and use taxes are calculated and paid. The form can be obtained from the Nebraska Department of Revenue or the county treasurer where the vehicle will be registered.

To calculate the sales tax due, follow these steps:

Remember to include a tire fee if applicable, which is calculated based on the number of new tires purchased.

If the total taxes and tire fee are not paid within 30 days of the purchase date, penalties and interest will be assessed. The county treasurer or designated official will collect these amounts at the statutory rate. It is crucial to pay on time to avoid additional costs. If the due date falls on a weekend or holiday, payment can be made on the next business day without incurring penalties.

Yes, certain exemptions apply to vehicle purchases in Nebraska. For instance, purchases made by exempt organizations or disabled persons with funds from specific government departments may qualify for exemptions. Additionally, vehicles used in specific capacities, such as common carriers, may also be exempt. To claim an exemption, the appropriate section of the Nebraska Resale or Exempt Sale Certificate must be completed, and supporting documentation should be provided. If documentation is insufficient, the tax may still be collected at the time of registration.

Sales Tax Exemption Certificate: Similar to the Nebraska Sales Tax Statement, this document is used to claim exemption from sales tax for certain purchases. It requires information about the buyer and the reason for the exemption, ensuring compliance with tax regulations.

Vehicle Title Application: This form is necessary for registering a vehicle. Like the Sales Tax Statement, it collects essential details about the vehicle and its owner, ensuring that the registration process is complete and accurate.

Bill of Sale: A bill of sale serves as proof of purchase for a vehicle. It shares similarities with the Sales Tax Statement in that it includes the buyer's and seller's information, vehicle details, and the purchase price, establishing a legal record of the transaction.

IRS W-9 Form: This form is crucial for providing your Taxpayer Identification Number (TIN) to avoid tax reporting issues. Like the Sales Tax Statement, it ensures compliance with tax regulations; to learn more about this process, visit PDF Templates.

Motor Vehicle Registration Application: This document is used to register a vehicle with the state. It parallels the Sales Tax Statement by requiring identification of the vehicle and the purchaser, ensuring that all necessary information is provided for registration.

Trade-in Allowance Form: This form is utilized when a vehicle is traded in as part of a purchase. Like the Sales Tax Statement, it calculates the value of the trade-in and reduces the taxable amount for the new vehicle, ensuring accurate tax computation.

Sales Tax Return Form: This form is filed by sellers to report collected sales tax. It is similar to the Sales Tax Statement in that it calculates tax based on sales, ensuring compliance with state tax obligations.

Application for Title and Registration: This document is essential for obtaining a vehicle title and registration. It is similar to the Sales Tax Statement in that it collects necessary information about the vehicle and its owner for official records.

Affidavit of Ownership: This form may be used when the original title is lost. It requires similar information to the Sales Tax Statement, affirming ownership and facilitating the title replacement process.

Motor Vehicle Use Tax Form: This document is used to report use tax for vehicles purchased out of state. It resembles the Sales Tax Statement by calculating tax based on the vehicle's purchase price and ensuring compliance with state tax laws.

Application for Exemption from Sales Tax: This form is used by certain organizations to apply for sales tax exemptions. Like the Sales Tax Statement, it requires detailed information about the buyer and the basis for the exemption.

The Nebraska Sales Tax Statement form is an essential document for anyone selling a motor vehicle or trailer in the state. However, it is often accompanied by other important forms and documents that help ensure compliance with state tax laws. Below is a list of related documents frequently used in conjunction with the Nebraska Sales Tax Statement.

Understanding these forms and their purposes can simplify the process of buying or selling a vehicle in Nebraska. Properly completing and submitting the necessary documents helps ensure compliance with tax laws, avoiding potential penalties or complications down the road.

Nebraska Form 13 - Form 17 must be retained by both the governmental unit and the prime contractor for records.

To ensure that your preferences are respected, it is vital to consider the importance of the Washington Durable Power of Attorney form in managing your affairs effectively.

How to Avoid Underpayment Penalty - Line 3 involves subtracting any refundable child or dependent care credits from your total tax figure.

Nebraska Tax Id Number Lookup - Select the type of ownership for your business.